Still relying on slow, outdated banking systems for international transactions? You’re leaving growth on the table.

The landscape of global commerce is shifting faster than ever. With cross-border business becoming the norm, companies can’t afford to be slowed down by traditional payment systems that come with high fees, delayed transfers, and complex compliance processes.

Enter the Digital Payment Gateway—a modern infrastructure that is redefining how global business payments are made.

Whether you’re an eCommerce brand, SaaS company, service-based agency, or global supplier, a Digital Payment Gateway is no longer optional—it’s essential to unlocking speed, security, and scale in your international operations.

This blog explores how these gateways work, what features matter, and how platforms like PayXBorder are leading the transformation.

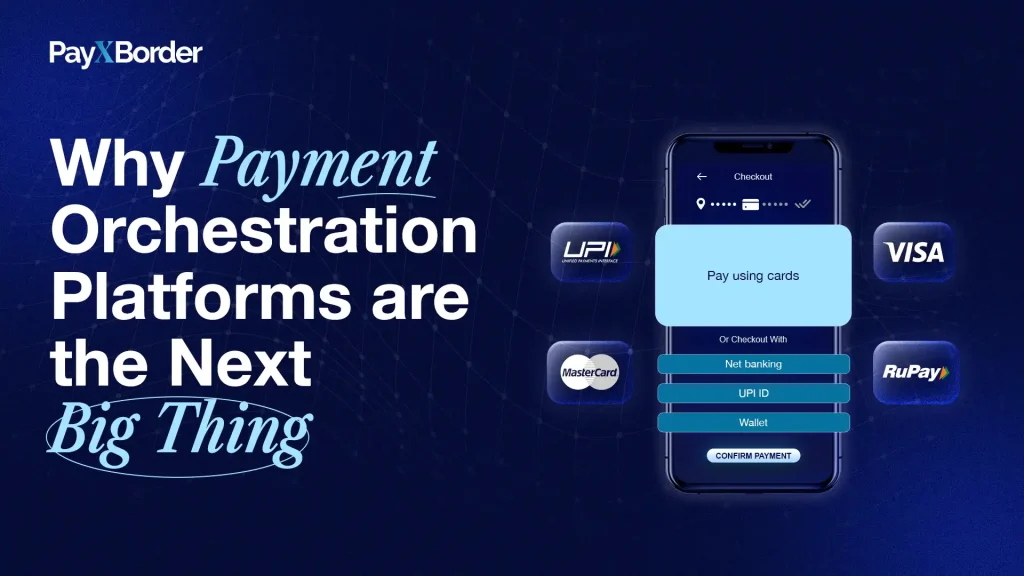

What is a Digital Payment Gateway?

A Digital Payment Gateway is an online technology solution that authorizes and processes payments across geographies, currencies, and platforms. It connects a merchant or business to global payment networks, banks, and financial institutions—while securing and facilitating seamless transactions.

These gateways are the backbone of international eCommerce and B2B payments, supporting functions such as:

- Multi-currency processing

- Fraud prevention & compliance

- Currency conversion

- Real-time settlements

- Payment reconciliation

- Wallet-to-wallet transfers

Key Benefits of Using a Digital Payment Gateway in Global Business

1. Speed & Efficiency

Traditional bank wires take days. A Digital Payment Gateway can settle transactions in minutes. This speed improves cash flow, accelerates delivery cycles, and reduces the time between order and fulfillment.

2. Transparent FX and Pricing

Global payments often come with hidden charges. Gateways like PayXBorder use real-time FX rates and a flat-fee model, eliminating surprises.

3. Enhanced Security & Compliance

With built-in features like AML screening, KYC verification, PCI-DSS security, and GDPR compliance, a reliable gateway ensures every transaction is secure and legally sound.

4. Localized Customer Experience

From language preferences to preferred payment methods (UPI in India, iDEAL in the Netherlands, Alipay in China), a digital gateway offers regional customization—critical for customer satisfaction and conversions.

5. Real-Time Tracking & Reporting

Monitor your global transactions through a live dashboard. Get alerts, reports, and forecasts to drive smarter financial decisions.

6. Developer-Friendly API Integrations

Connect payment processing with your ERP, accounting software, or marketplace through plug-and-play APIs for seamless workflow automation.

Top Use Cases for Digital Payment Gateways in Business

eCommerce

Offer checkout in local currencies, reduce cart abandonment, and accept global payments with ease.

Freelancing & Contracting

Enable international clients to pay freelancers in their preferred currency—instantly.

Import/Export Businesses

Pay global vendors and receive export payments with fast settlements and reduced FX loss.

SaaS Subscriptions

Bill customers in different geographies with recurring subscription options and local payment support.

Travel & Hospitality

Accept bookings globally and settle faster with multi-currency tools.

What to Look for in a Digital Payment Gateway

- Real-Time FX Conversion

- Multi-Currency Wallet Support

- Instant Wallet-to-Wallet Transfers

- Regulatory Compliance (AML, KYC, PCI, GDPR)

- Developer Documentation for API Integration

- Transparent Pricing with No Hidden Fees

- 24/7 Global Support

- Automated Reconciliation Tools

How PayXBorder is Driving the Digital Payment Gateway Revolution

PayXBorder is one of the few platforms that has re-engineered global payments with an all-in-one solution for businesses. It provides:

- Flat Fee Setup: Pay once, transact freely without hidden deductions.

- Live Currency Exchange: Get competitive, mid-market FX rates with each transaction.

- Multi-Currency Wallet: Hold, send, and receive over 50+ global currencies.

- Instant Transfers: Wallet-to-wallet transactions within seconds.

- Compliance-First Framework: Full AML, KYC, GDPR, and PCI-DSS built-in.

- API Integrations: Easily connect with your business stack (ERPs, CRMs, eCommerce platforms).

- Insightful Dashboards: Track and analyze payment trends, success rates, and FX exposure.

Whether you’re scaling across borders or just getting started, PayXBorder helps you gain control, reduce costs, and streamline global payments.

Common Myths About Digital Payment Gateways

Myth 1: Digital gateways are only for large enterprises.

Reality: Platforms like PayXBorder serve freelancers, startups, and SMBs just as effectively.

Myth 2: You still need traditional banks for large transfers.

Reality: Most digital gateways can process large volume payments faster and cheaper than banks.

Myth 3: Compliance is complicated.

Reality: With a gateway that automates AML, KYC, and reporting, compliance becomes seamless.

Myth 4: Digital gateways are not secure.

Reality: Top platforms follow global financial security standards such as PCI-DSS and GDPR.

Final Thoughts: Powering the Future of Global Payments

In 2025 and beyond, global business requires speed, flexibility, and transparency. The Digital Payment Gateway is no longer just an IT feature—it’s a strategic business tool.

Companies using platforms like PayXBorder are saving on fees, accelerating growth, and offering better global customer experiences.

Don’t let old systems slow you down. Power your global payments with PayXBorder.