Still relying on traditional bank transfers for your global business? You might already be falling behind.

In today’s fast-paced digital economy, businesses operating internationally are under pressure to be faster, more flexible, and more inclusive than ever before. Traditional banking systems, with their slow settlements, high fees, and limited accessibility, are no longer cutting it. That’s where Alternative Payment Methods (APMs) come in.

From mobile wallets to blockchain-based transfers, APMs are not just convenient add-ons—they are becoming the backbone of international business transactions. Whether you’re a freelancer in India working with a client in Germany or a SaaS startup in Singapore onboarding users from the U.S., choosing the right payment method can make or break your deal.

This blog explores the transformative role of Alternative Payment Methods and why platforms like PayXBorder are driving this change for businesses across the globe.

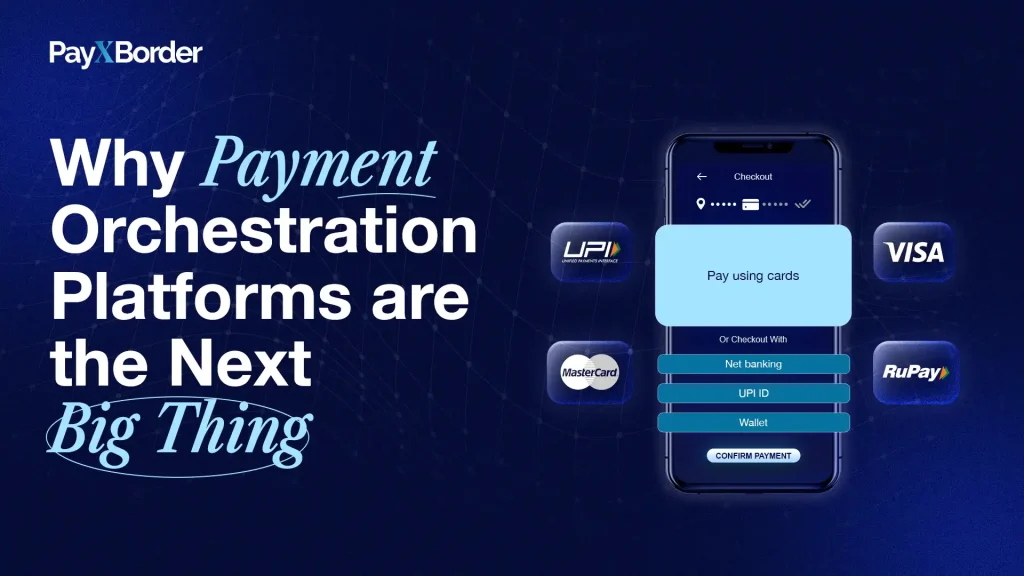

What Are Alternative Payment Methods?

Alternative Payment Methods (APMs) are non-traditional payment solutions that provide options beyond credit/debit cards and wire transfers. They include:

- E-wallets (PayPal, Skrill, Alipay)

- Buy Now, Pay Later (BNPL) solutions (Klarna, Afterpay)

- Mobile payments (Apple Pay, Google Pay)

- Cryptocurrencies

- Instant bank payments (UPI, SEPA Instant)

- Cross-border digital platforms like PayXBorder

These methods are faster, more accessible, and often cheaper than traditional banks, especially for international transactions.

Why the Surge in APMs?

Frictionless Experience

Customers want instant, smooth transactions without filling out lengthy banking forms or waiting for 3-5 business days.

Financial Inclusion

Billions of users globally don’t have access to traditional banking but do use mobile wallets or digital apps.

Rising eCommerce & Freelance Economy

Global online sales and digital work have exploded, requiring flexible payment systems that work across borders.

Security and Control

Many APMs offer greater transaction transparency, security layers, and real-time tracking.

The Impact of Alternative Payment Methods on International Business

1. Breaking Down Borders

Businesses can now operate across continents without worrying about slow wire transfers or incompatible banking systems. With APMs like PayXBorder, companies can:

- Instantly pay vendors in multiple currencies

- Accept client payments globally without currency issues

- Offer customers local payment options

This builds trust and accelerates deal closures.

2. Lowering Operational Costs

Traditional banks often charge:

- Hidden fees

- High foreign exchange (FX) margins

- Intermediary charges

Alternative Payment Methods reduce or eliminate many of these. Platforms like PayXBorder offer flat-fee structures, competitive FX rates, and no surprise costs.

3. Improving Cash Flow

Fast settlement means businesses don’t have to wait days or weeks to access funds. This improves liquidity, enabling quicker reinvestment and scaling.

4. Increasing Customer Conversion Rates

Offering multiple local and digital payment methods increases the likelihood of a sale. If users can’t pay the way they want, they won’t complete the purchase.

APMs empower businesses to offer a seamless checkout experience regardless of the buyer’s geography.

How PayXBorder Supports Alternative Payment Methods

PayXBorder is more than a payment solution—it’s a global transaction enabler.

Here’s how it supports APM adoption:

Multi-Currency Wallet

Businesses can receive, hold, and send payments in multiple currencies—without constantly converting funds.

Virtual IBANs

PayXBorder provides localized banking experiences in multiple countries, making cross-border payments feel local.

Transparent Pricing

There are no hidden charges. Businesses know exactly what they’re paying before a transaction is processed.

Developer-Friendly APIs

Businesses can integrate APMs into their platforms using PayXBorder’s APIs, supporting seamless user journeys.

Instant Settlements

Unlike traditional banking, PayXBorder enables faster settlements, helping businesses operate in real time.

Types of Alternative Payment Methods in International Trade

Mobile Wallets

Used globally and offer quick QR-code-based or app-based transactions.

Crypto Payments

Especially popular in regions with unstable local currencies. Bitcoin, USDT, and Ethereum are top choices.

Cross-Border Fintech Platforms

Platforms like PayXBorder are ideal for B2B payments, freelancer payouts, and vendor settlements.

BNPL for B2B

Emerging as a way to offer business buyers flexible payment terms, improving purchasing power.

Challenges Faced by Businesses Without APMs

Businesses not adopting Alternative Payment Methods risk:

- Lost customers due to poor payment experience

- High costs from traditional wire transfers

- Delayed transactions impacting operations

- Non-compliance with modern regulatory expectations

- Limited reach in underbanked markets

APMs are no longer optional—they’re essential.

Benefits of Alternative Payment Methods for B2B Businesses

- Faster invoicing and settlement cycles

- Reduced cart abandonment in SaaS and eCommerce

- Simplified compliance with international regulations

- Better cash flow forecasting

- Global scalability without changing core infrastructure

For B2B exporters, digital agencies, SaaS providers, and international consultants, switching to APMs through PayXBorder can be a game-changer.

Future Trends in Alternative Payment Methods

Embedded Finance

APMs will become part of the service flow rather than external options—think Uber integrating payments within the app.

AI-Driven Fraud Detection

Smarter fraud tools will be embedded in payment platforms.

Real-Time Global Payments

Instant money transfers across countries will become the norm, reducing reliance on SWIFT or intermediary banks.

CBDCs (Central Bank Digital Currencies)

Several countries are already experimenting with digital currencies for secure and transparent payments.

How to Choose the Right Alternative Payment Partner

Before integrating any APM, assess:

- Regulatory compliance (AML, KYC, GDPR)

- Security (End-to-End Encryption, 2FA)

- Settlement time

- Fees and FX transparency

- Developer tools for integration

- Reputation and support

PayXBorder ticks all these boxes while providing a user-friendly dashboard and instant onboarding process.

Voice Search Optimized FAQs

1. What are alternative payment methods?

They are non-traditional ways to send or receive money like wallets, mobile payments, or fintech platforms.

2. Why are alternative payment methods important for global business?

They allow faster, cheaper, and more flexible transactions across borders, improving efficiency.

3. Is PayXBorder an alternative payment method?

Yes, PayXBorder is a digital platform that supports multiple APMs for secure cross-border transactions.

4. What is the safest alternative payment method?

Digital platforms with compliance, encryption, and fraud monitoring—like PayXBorder—offer top-tier safety.

5. How do APMs improve international payments?

They reduce costs, speed up settlements, and offer better options for global clients and partners.