In today’s globalized economy, cross-border transactions are not just for large corporations; small businesses, freelancers, and even individuals regularly make international payments. Whether it’s paying suppliers overseas or sending money to family across borders, one thing is certain: costs can quickly add up. From hidden fees to inflated currency exchange rates, cross-border payments can become an expensive affair.

However, with careful planning and smart choices, you can significantly reduce these costs and save thousands over time. In this guide, we’ll explore how you can make low-cost cross-border transfers, why it’s so important in the current financial landscape, and what trends and challenges the industry is currently facing. By the end, you’ll have actionable strategies for minimizing fees and maximizing the value of your international payments.

Why Low-Cost Cross-Border Transfers Matter

Cross-border payments play a pivotal role in global trade and finance. They allow businesses to operate internationally, individuals to send remittances, and global economies to function seamlessly. Yet, the fees associated with these transfers can often be prohibitively high, impacting both businesses and individuals alike.

In the context of global trade, the cost of making frequent international payments can cut into profit margins, slow down transactions, and complicate financial planning. For individuals sending remittances to support family members abroad, high fees mean less money is received by their loved ones.

Lowering the cost of cross-border transfers has a ripple effect: it boosts global trade by reducing friction, makes remittances more efficient, and contributes to economic growth, especially in developing countries. This is why finding low-cost solutions for cross-border transfers is more important now than ever before.

The Hidden Costs of Cross-Border Payments

Before we dive into how to save money, it’s important to understand the types of fees that can make cross-border transfers expensive. Here are some common hidden costs:

- Transfer Fees: Many banks and traditional payment processors charge a flat fee for sending money internationally, which can range from $10 to $50 or more per transaction.

- Currency Conversion Fees: Some providers charge a hidden markup on the exchange rate, which means you receive less money than expected when converting currencies.

- Intermediary Bank Fees: For international payments made through the SWIFT network, multiple intermediary banks may process the transfer, each deducting their own fees.

- SWIFT Charges: In certain cases, the bank receiving the payment might also charge fees for processing SWIFT transfers, further reducing the amount the recipient receives.

- Delayed Settlement Fees: For payments that take longer to process, some payment platforms may apply additional fees for faster service.

These fees, often not disclosed upfront, can add up over multiple transactions and result in substantial costs over time. Fortunately, new innovations in the cross-border payments industry are addressing these challenges.

Current Trends in Low-Cost Cross-Border Transfers

The cross-border payments landscape has evolved significantly in recent years, driven by technological advancements and a growing demand for cheaper, faster, and more transparent transfers. Here are some of the current trends making waves in the industry:

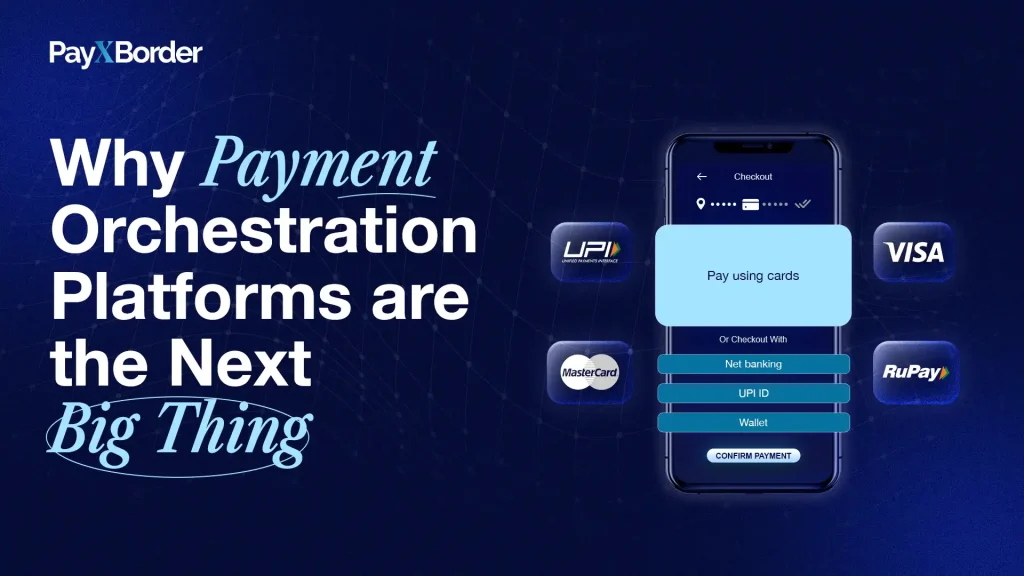

- Fintech Disruption: Fintech companies are leading the charge in offering low-cost, high-speed cross-border transfer services. Platforms like TransferWise (now Wise), Revolut, and PayXBorder are providing alternatives to traditional banks by offering real-time exchange rates and low fees.

- Blockchain and Cryptocurrencies: Blockchain technology is revolutionizing cross-border payments by enabling decentralized, near-instant transfers with minimal fees. Cryptocurrencies like Bitcoin and stablecoins such as USDT are also gaining popularity as payment methods, reducing reliance on traditional banking systems.

- Digital Wallets: Wallet-to-wallet transfers are emerging as a cost-effective solution for cross-border payments. Services that allow direct wallet-to-wallet transfers, such as PayXBorder, provide a low-fee alternative to traditional methods.

- AI and Automation: Many fintech platforms are integrating AI-powered tools for real-time fraud detection, AML (Anti-Money Laundering) checks, and transaction monitoring. These advancements ensure compliance while reducing the cost of manual oversight, translating into lower fees for users.

How to Save Thousands: Practical Solutions

Now that we’ve covered why low-cost cross-border payments are so important, let’s dive into the actionable steps you can take to minimize fees and save money.

1. Choose the Right Payment Provider

Traditional banks often charge higher fees and offer less favorable exchange rates than modern fintech solutions. Switching to a provider that specializes in low-cost international payments, such as PayXBorder, can help you avoid high fees and save on currency conversions.

2. Opt for Wallet-to-Wallet Transfers

Wallet-to-wallet transfers are typically faster and more cost-effective than traditional bank transfers. By keeping funds in a multi-currency digital wallet, you can send and receive payments across borders with minimal fees and better exchange rates.

3. Use Real-Time Currency Conversion Tools

Make sure your payment provider offers real-time currency conversion rates to avoid hidden markups. Some platforms, like PayXBorder, offer transparent, real-time currency conversion so you know exactly how much you’re sending and receiving.

4. Batch Payments

If your business makes frequent international payments, consider batching your transactions to save on fees. Many providers offer discounted rates for larger or grouped transactions, which can reduce the overall cost of sending money abroad.

5. Avoid SWIFT Fees

SWIFT fees can add up quickly, especially for large or frequent transactions. Look for providers that offer SWIFT alternatives, such as wallet-to-wallet transfers or localized payment networks, to avoid these fees altogether.

6. Compare Exchange Rates

Always compare exchange rates before making a cross-border payment. Even a small difference in the rate can result in significant savings when sending large sums of money. Choose a provider that offers mid-market exchange rates with no hidden markups.

7. Look for Flat-Fee Structures

Some providers, including PayXBorder, offer flat-fee pricing models. This makes it easier to calculate costs upfront and ensures you’re not hit with unexpected charges. A flat fee structure can be especially beneficial for businesses making regular payments abroad.

Challenges in the Cross-Border Payments Industry

While there are many ways to save on cross-border transfers, the industry still faces challenges. These include regulatory compliance issues, varying legal requirements across countries, and managing risks like fraud and money laundering.

Compliance with regulations such as Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements is essential but can increase operational costs. However, as technology evolves, AI and blockchain are helping businesses streamline compliance processes, making cross-border payments more efficient and secure.

Conclusion: Stay Informed and Save Big

In a globalized economy, making cross-border payments is inevitable, but high fees don’t have to be. By choosing the right provider, utilizing digital wallets, and taking advantage of transparent pricing models, you can save thousands on cross-border transfers.

As the industry continues to evolve, staying informed about trends and innovations in fintech can help you make smarter financial decisions. Companies like PayXBorder are leading the way in providing cost-effective, transparent, and secure solutions for international payments.