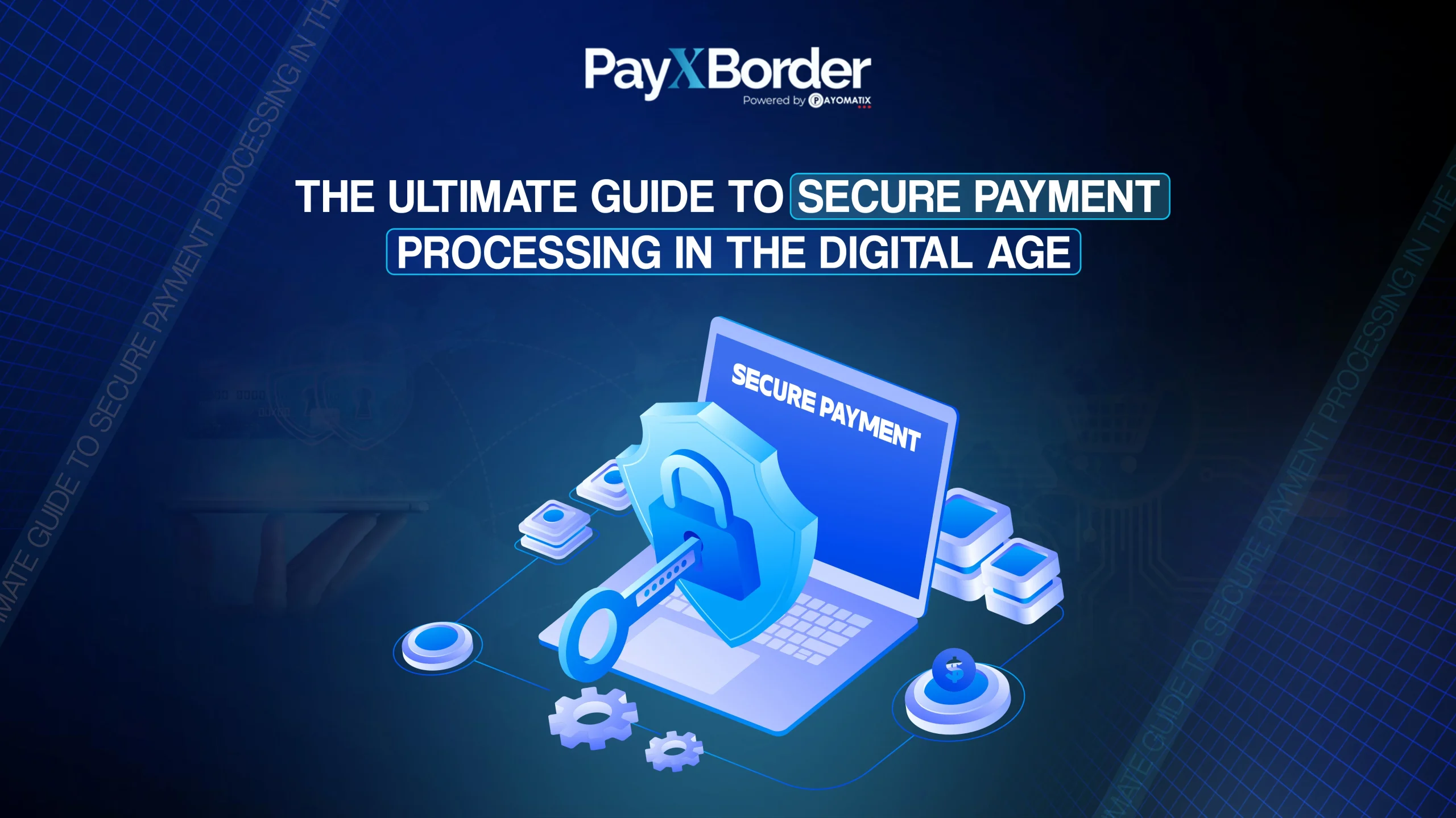

Ever felt nervous sending payments across borders or collecting money online? In today’s digital world, secure payment processing is not just a luxury—it’s a necessity.

As global commerce becomes increasingly digital and decentralized, ensuring the safety of your financial transactions is more crucial than ever. Every online business, freelancer, exporter, and digital entrepreneur must prioritize Secure Payment Processing to protect their revenue, reputation, and customer trust.

From eCommerce giants to emerging startups, one data breach or fraudulent transaction can cripple business operations. The solution? Adopting robust, scalable, and intelligent payment systems built for modern threats and international needs.

This ultimate guide dives deep into the world of Secure Payment Processing—covering how it works, why it matters, the latest technologies behind it, and why platforms like PayXBorder are setting new standards for global security in digital payments.

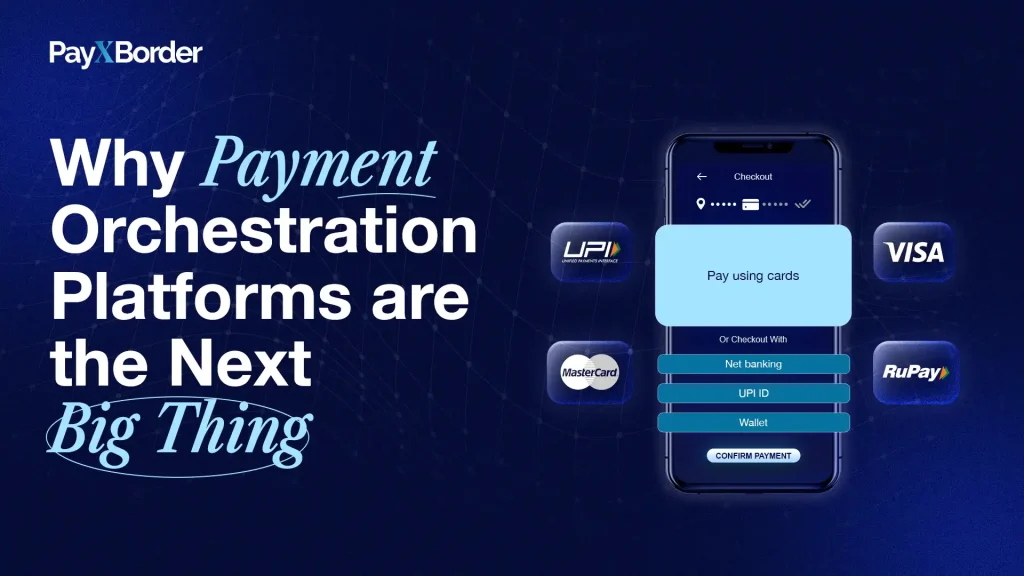

What is Secure Payment Processing?

Secure Payment Processing refers to the safe transfer, authorization, and settlement of financial transactions through online platforms while ensuring data confidentiality, integrity, and compliance with security standards like PCI DSS, AML, and KYC.

It involves encryption, tokenization, fraud detection, and real-time monitoring to make sure your money moves safely from sender to receiver without risk of interception or manipulation.

In the digital age, where cross-border payments are the norm, security must be built into the core of every transaction—not added as an afterthought.

Why Secure Payment Processing Matters in 2025

With cyber threats at an all-time high and international regulations tightening, secure payment infrastructures are critical to:

- Prevent data breaches and financial fraud

- Ensure compliance with global financial regulations

- Safeguard customer trust and brand credibility

- Enable seamless global expansion

- Reduce chargebacks and transaction disputes

Security is no longer just the IT department’s concern—it’s a business driver. Without secure systems, global commerce cannot thrive.

Threats That Make Secure Payment Processing Essential

Understanding the risks involved helps businesses appreciate the value of robust payment security:

1. Data Breaches

Hackers can exploit weak payment systems to access sensitive financial data, customer identities, and login credentials—leading to massive financial and reputational losses.

2. Phishing & Spoofing

Fake payment requests and duplicate websites can trick users into providing card details or credentials to fraudsters.

3. Payment Interception

Man-in-the-middle attacks during payment transmission can allow unauthorized parties to manipulate transactions.

4. Internal Fraud

Employee misuse of admin access or business data poses an equally dangerous threat if access isn’t properly segmented and monitored.

What Makes a Payment System “Secure”?

Here are the core elements that every Secure Payment Processing system must include:

End-to-End Encryption (E2EE)

Protects data in transit—ensuring only the intended parties can access the payment information.

Tokenization

Replaces sensitive data (like card numbers) with non-sensitive tokens during storage and transmission.

Real-Time Fraud Detection

Uses AI and machine learning to detect and stop suspicious transactions as they happen.

Compliance Protocols

Ensures that the system adheres to global standards such as:

- PCI DSS (Payment Card Industry Data Security Standard)

- AML (Anti-Money Laundering)

- KYC (Know Your Customer)

- GDPR for data privacy

Multi-Factor Authentication (MFA)

Adds another layer of security by requiring additional verification from users.

How PayXBorder Ensures Secure Payment Processing

As a global payment solution built for cross-border transactions, PayXBorder places security at the core of its operations. Here’s how:

1. Military-Grade Encryption

All data transmitted and stored via PayXBorder is protected using AES-256 encryption, the gold standard in data security.

2. Instant Transaction Alerts

Users receive real-time notifications of all incoming and outgoing payments—helping detect suspicious activity instantly.

3. AML & KYC Compliance

PayXBorder’s onboarding process includes automated verification and document checks that meet FATF recommendations, keeping the platform compliant globally.

4. Role-Based Access Control

Accounts are segmented by roles—ensuring that only authorized users can approve, view, or send transactions.

5. Secure APIs for Integration

Developers and platforms can safely integrate PayXBorder’s services via encrypted APIs with OAuth authentication protocols.

PayXBorder is not just a payment gateway—it’s a digital vault for your global transactions.

Top Technologies Driving Secure Payment Processing

As cybercriminals evolve, so must payment platforms. Here are the leading technologies shaping secure processing today:

Blockchain

By decentralizing transaction records and encrypting them immutably, blockchain adds unparalleled transparency and trust to payment processing.

AI & Machine Learning

From fraud detection to transaction pattern recognition, AI helps identify and stop threats in real-time.

Biometric Verification

Fingerprint and facial recognition features are becoming more common for authenticating payments, especially on mobile.

Cloud Infrastructure Security

Modern platforms use highly secure cloud servers with built-in redundancy and automatic security patching.

Best Practices for Businesses to Ensure Secure Payment Processing

Even with a secure platform, businesses must adopt smart payment hygiene:

- Use PCI-DSS compliant service providers

- Regularly update software and payment plugins

- Educate staff on social engineering and phishing

- Avoid storing cardholder data unnecessarily

- Enable 2FA on all admin portals

- Conduct quarterly security audits

The more proactive your approach, the safer your ecosystem.

Common Mistakes That Compromise Payment Security

- Using outdated plugins or CMS platforms

- Storing unencrypted cardholder data

- Ignoring multi-factor authentication

- Partnering with unverified payment providers

- Sharing admin credentials across departments

Avoiding these can significantly reduce the chances of a payment-related breach.

Why Secure Payment Processing is Key to Global Growth

Businesses operating across countries face complex regulatory frameworks. With Secure Payment Processing, companies can:

- Accept payments from customers in multiple countries

- Avoid penalties from non-compliance

- Protect sensitive cross-border financial data

- Build customer trust across regions

- Streamline operations with centralized control

Platforms like PayXBorder enable this by combining global infrastructure with next-level security.

How to Choose the Right Secure Payment Platform

Here’s what to look for in a solution:

- Global Compliance Certifications

- End-to-End Encryption and Tokenization

- Transparent Fee Structure

- Instant Payment Tracking

- Real-Time Security Alerts

- Multi-Currency Support

- Developer API Access

PayXBorder checks all these boxes—making it an ideal choice for businesses serious about growth and security.

Voice Search Optimized FAQs

1. What is secure payment processing?

Secure payment processing is a method of transferring money online while protecting sensitive data through encryption, tokenization, and compliance standards.

2. Why is secure payment processing important?

It protects your business and customers from fraud, data breaches, and financial losses during online transactions.

3. How does PayXBorder ensure payment security?

PayXBorder uses AES-256 encryption, real-time alerts, AML/KYC compliance, and role-based access to protect your global transactions.

4. What are the risks of insecure payment processing?

You could face data breaches, fraudulent transactions, regulatory fines, and loss of customer trust.5. How can businesses improve payment security?

Use PCI-compliant platforms, enable 2FA, keep systems updated, and educate teams on cyber threats.