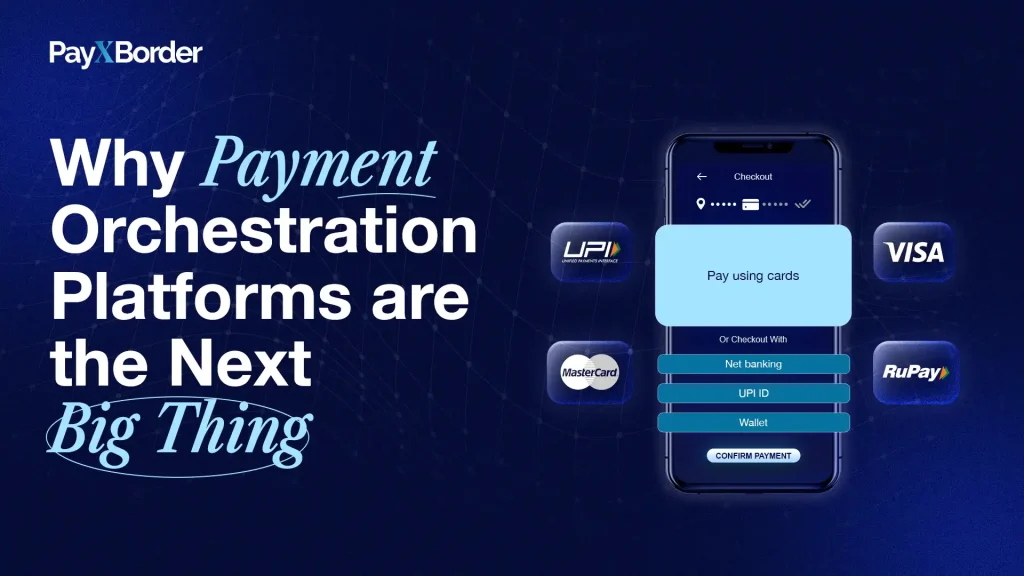

Introduction

International remittance refers to the process of sending money across national borders, typically from individuals working abroad to family members or loved ones in their home countries. This financial flow has become a crucial source of income for millions of families globally, particularly in low- and middle-income countries. According to World Bank data, global remittances reached $540 billion in 2020, and this figure continues to grow as the global workforce becomes increasingly mobile.

International remittances play a vital role in promoting financial inclusion, reducing poverty, and boosting the economy in recipient countries. In fact, for many families, remittances are lifelines, helping to cover daily expenses, education, healthcare, and even entrepreneurial ventures. This article will provide a comprehensive overview of what international remittance is, how it works, the mechanisms involved, and the benefits and challenges surrounding it.

What Is International Remittance?

International remittance is the transfer of money by an individual in one country to recipients in another country, usually family members or dependents. These transfers are typically made by migrants or expatriates who are working in foreign countries and sending part of their earnings back home.

For instance, a nurse working in the United States might regularly send a portion of her salary to her family in the Philippines. These remittances help the family cover living costs, education, and medical expenses. In many developing nations, international remittances account for a significant percentage of the national GDP, sometimes exceeding foreign direct investment (FDI) and official development assistance (ODA).

Key Statistics:

- World Bank estimates suggest that international remittances to low- and middle-income countries will surpass $750 billion by 2023.

- Countries like India, Mexico, the Philippines, and China are among the top recipients of remittances globally, with India receiving a staggering $89 billion in 2021.

How Does International Remittance Work?

International remittance services enable the seamless transfer of money across borders, but the process is not as straightforward as domestic transfers. The remittance process involves multiple parties and steps, and several channels can be used depending on the sender’s and recipient’s preferences. Here’s how international remittances generally work:

1. Selection of a Remittance Provider

To send money internationally, individuals must first choose a remittance provider. This can be a bank, a money transfer operator (MTO) like Western Union or MoneyGram, or a digital wallet service like PayPal, TransferWise (now Wise), or Revolut. Each provider offers different services, fees, and delivery times, so choosing the right provider is essential based on cost, speed, and convenience.

2. Transfer of Funds

Once the remittance provider is selected, the sender initiates the transfer by providing necessary details, such as:

- Recipient’s information (name, location, and sometimes account number or phone number for digital wallets).

- Amount to be sent and currency choice (many remittance providers allow you to choose the currency for the transfer).

- Payment method (bank transfer, cash deposit, credit/debit card, or online payment gateway).

The funds are then sent from the sender’s account to the remittance provider, who facilitates the transfer.

3. Currency Conversion

Since the sender and recipient often deal with different currencies, the remittance provider typically converts the money into the recipient’s local currency. Currency exchange rates are a crucial factor in determining the final amount the recipient will receive. Providers usually charge an exchange rate margin or a fee for this service.

4. Delivery to Recipient

Once the funds are processed, they are delivered to the recipient. Delivery methods vary, including:

- Bank account deposit: The money is deposited directly into the recipient’s bank account.

- Cash pickup: The recipient can pick up cash from an authorized agent or branch, such as Western Union locations.

- Mobile wallets: Increasingly, remittances are being sent to mobile wallets, which recipients can access through their phones.

- Door-to-door delivery: In some countries, cash delivery services are available for those unable to visit a collection point.

5. Confirmation and Tracking

The sender usually receives confirmation of the transaction, either through email, SMS, or app notifications. Many modern remittance providers also offer tracking services so that the sender can monitor the progress of the transfer in real time.

Key Benefits of International Remittance

1. Poverty Reduction and Economic Impact

One of the primary benefits of international remittances is poverty alleviation. In countries like the Philippines and Nigeria, remittances provide families with a stable source of income that they can use for basic necessities. Studies have shown that remittances often lead to better access to healthcare, education, and housing for recipients. In some cases, remittances can even spur small-scale investments and entrepreneurship.

According to the International Monetary Fund (IMF), remittances contributed to reducing poverty levels by 11% in sub-Saharan Africa between 2000 and 2017.

2. Financial Inclusion

Remittances often promote financial inclusion by integrating more people into the formal financial system. Many recipients open bank accounts to receive remittances, thus becoming part of the formal financial sector. This integration can offer them access to other financial products, such as savings accounts and credit, empowering them to manage their money more efficiently.

3. Foreign Exchange Boost

For recipient countries, remittances are a valuable source of foreign exchange, helping to stabilize local currencies and improve the balance of payments. This is especially crucial for nations that rely heavily on remittance inflows, such as Bangladesh, where remittances account for more than 6% of the GDP.

Challenges and Issues in International Remittance

1. High Transaction Costs

One of the significant challenges in international remittance is the cost of sending money across borders. According to the World Bank’s Remittance Prices Worldwide Database, the average cost of sending remittances globally was 6.5% in 2020. For many low-income migrants, this fee is prohibitive, especially when sending smaller amounts. Reducing these costs is critical to maximizing the positive impact of remittances on recipient families.

2. Slow Transfer Times

While some modern remittance services can process transfers in minutes, others can take several days. Traditional banking channels often involve lengthy processes, especially for countries with underdeveloped financial infrastructures. Delays can be a significant issue when recipients rely on the money for urgent needs.

3. Regulatory Barriers

International remittance services must comply with a host of regulations, including Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements. These rules are in place to prevent illegal activities, but they can make the remittance process more cumbersome and expensive, especially for senders in countries with stringent regulatory frameworks.

4. Exchange Rate Fluctuations

Exchange rate volatility can affect the final amount received in remittances, as transfer companies often charge a markup on currency conversions. This can reduce the purchasing power of remitted funds, particularly in economies with rapidly depreciating currencies.

Real-World Example: International Remittances in India

India is the world’s largest recipient of international remittances, with total inflows reaching $89 billion in 2021. Remittances account for nearly 3% of India’s GDP, and they provide crucial support to families in rural areas, where many depend on money sent by relatives working in the Middle East, the U.S., and Europe.

During the COVID-19 pandemic, remittances proved to be a stabilizing force for the Indian economy, even when other sources of foreign exchange, such as tourism and exports, declined. Kerala, a state heavily reliant on remittances from its diaspora in the Gulf region, witnessed firsthand the importance of international remittance as workers sent funds to support families amid the economic crisis.

Conclusion and Future Trends

International remittance is a vital financial flow that has a far-reaching impact on global poverty alleviation, economic growth, and financial inclusion. With technology continuing to advance, the remittance landscape is evolving, becoming faster, cheaper, and more accessible. Emerging technologies like blockchain and cryptocurrency have the potential to further reduce costs and improve security, while fintech innovations are simplifying the user experience.

As cross-border payments become increasingly digital, it is likely that remittances will continue to grow in importance, especially as more people migrate for work and global economies become more interconnected. Governments, financial institutions, and fintech companies will need to collaborate to ensure that remittance services remain affordable, transparent, and secure for the millions of people who depend on them.

In the future, we can expect to see greater integration of digital wallets, real-time payments, and mobile banking, making remittances faster and more accessible to even the most remote communities. Reducing transaction costs and improving transparency will be critical to unlocking the full potential of international remittances in driving sustainable development and financial inclusion across the globe.